Liability Insurance for Child-Serving Organizations

Exactly nobody's favorite topic

Insurance has always been a challenge for Skookum Kids, the foster care organization I founded and lead. When I paid our premiums in the first year, it was the single biggest check I had ever written. In the 12 years since, our liability insurance premiums have increased by more than 300%. Despite never having made an insurance claim (ever, of any kind or size), there have been multiple points in our history when I believed we might have to cease operations for want of an insurance underwriter who would cover us.

So what’s going on here? Why is it so hard and costly for a mid-sized child-serving organization to buy standard liability insurance? It’s a systemic problem. Solving it will require a cold-hearted pragmatism that flies in the face of values that even I—a committed pragmatist—hold dear.

How insurance works

Insurance is an instrument to amortize risk over time. A car accident can lead to high costs. This includes repairs to your car, medical bills, and damage to other cars. While it may not always be catastrophic, it certainly can be. Most car accidents are not catastrophically expensive but swerving to miss a deer and instead hitting a Lamborghini Huracan would be! That bill could bankrupt someone and/or leave damage, especially to the Huracan or the people inside it, unrepaired. Instead of running the risk that a car accident bill might be financially ruinous, insurance trades that risk for a fixed monthly price. Insurance does not reduce the risk of a car accident, but it functionally eliminates the risk that the cost of an accident could be financially ruinous. In most places, making this trade is not optional. Car insurance is required by law. This is mainly due to the risk that cars pose to others and their property.

Insurance is also a business. In exchange for collecting that monthly price, Insurance companies promise to pay for rare, catastrophically expensive car accidents. This promise is written into a contract. To set their prices, insurance providers do some arithmetic about how costly and how frequent car accidents are. Premium volume, which is the revenue of an insurance company, must be higher than payouts, or expenditures, by a significant margin for insurance to exist. If it is not, the insurance market will not function. Said another way: if car accidents become much more common or more costly on average, the price of insurance goes up.

You know all that. You are an adult who reads long explainers on the internet. Of course, you know how insurance and the insurance marketplace works. The problem is: the people setting the policies that have all but destroyed the insurance market for child-serving organizations are also adults who read long explainers on the internet. But somewhere along the way these facts have been overridden by societal values about justice.

Why Skookum’s insurance is so expensive

In much the same way that a car can be dangerous to pedestrians and other motorists, a child-serving organization can be dangerous to operate too. Skookum Kids is a child welfare organization. We care a lot about preventing and helping children heal from the evils of abuse and neglect. And it is just an uncomfortable fact that predators are drawn to places where children congregate. We work hard to keep people safe in our programs. We use background checks, training, and strict policies to stop those with bad intentions. We’re always looking for ways to improve safety even more. But no system is perfect, and for any organization that serves children, managing risk will be a constant project. For what it’s worth, I think the most dangerous organizations are those operated by people who deny that fact.

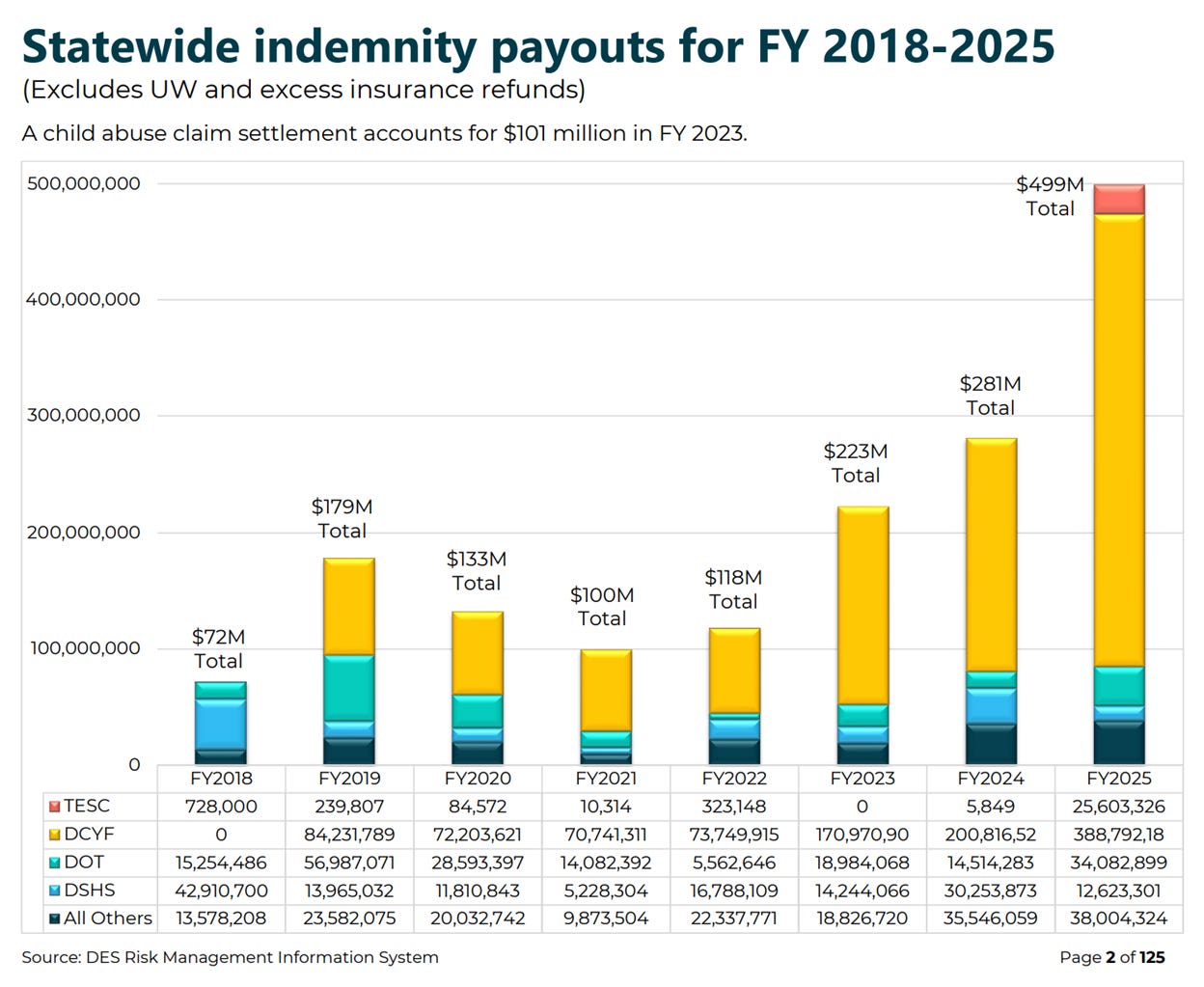

So, just like cars, Skookum and nearly all child-serving organizations must buy specific types and amounts of insurance. The price of that insurance is the product of an equation that accounts for size and likelihood of claims made, so any change in either the number of claims or the average claim size is going to affect the price of insurance. Tort claims paid by the state of Washington have reached a record high in each of the last 3 years, climbing to nearly $500m in FY2025.

Source: WA DES Tort Claim Analysis Report

The big yellow bar is tort liability paid by the Division of Children, Youth & Families (DCYF), the state agency responsible for childcare, foster care, and juvenile justice in our state. Tort payouts from the State of Washington differ from foster care-related payouts. Still, insurance companies may view them as similar enough to change their pricing.

Also, when DCYF contracts with a community-based organization like Skookum Kids to deliver a service to children and/or families impacted by foster care, they include language requiring our liability insurance to indemnify them. In other words, if a child in our care is harmed because a member of their staff acted in error (by withholding important information about the case, as a hypothetical example), our contract says that Skookum, not DCYF is liable. When I mention this to DCYF leaders, they assure me they do not intend to shift responsibility to my organization or others. Their legal team also confirms that this language shouldn’t have that effect. When DCYF is named in a lawsuit, they have a long history of bringing in any community-based organization that has a contractual obligation to indemnify them. In other words: I do not find their assurances credible.

It is reasonable to be alarmed while looking at that chart about the state of risk management at DCYF and among child-serving organizations across the state. The sudden rise in tort claims isn’t due to current events, as you and insurance providers might suspect. The overwhelming majority of these claims are from alleged events that happened decades ago. The driver is a series of legislative[1] and Supreme Court decisions[2][3] which have expanded the statute of limitations. Also, Washington is one of 28 states which have no cap on payouts of this kind, and the going rate keeps climbing.

This is not fun to talk about

I’ve accepted my lot in life to tackle unsavory and ethically complex issues. Tort liability from historic child sexual abuse might be the worst of these—or the best, depending on your perspective. There were and are instances of horrific abuse occurring in group homes and foster care, and the victims of that abuse deserve justice. Sometimes, the events aren’t just one mistake or a bad actor. They show a pattern that is systemic. One of the cases that I followed most closely in recent years was about Secret Harbor, a close partner agency of ours. The case describes a bygone phase of the organization’s history in which conditions for children were horrific. It reads like a catalog of every possible management failure, and the result is deplorable treatment of children. The organization described in that case should be shut down for good. However, that organization has not existed for a long time.

In 1990, a skilled leader took charge at Secret Harbor. He guided the organization through a major change. This included closing the Cypress Island facility, moving operations to the mainland, securing agency accreditation, and updating its program mix. Under that leader, Secret Harbor transformed into a standard-setting example of care. It helped a lot of kids and rightly elevated its staff into industry leadership, whom I was fortunate to meet and learn from. Like the Ship of Theseus, you would be hard-pressed to find any component from ‘Juvenile Alcatraz’ remaining in the Secret Harbor I knew and respected. The lawsuit, while justified in the eyes of every reasonable observer, did not have the effect of holding the bad actors accountable. The individuals responsible for that evil are long gone. But it did drive the organization I knew out of business because, after the case was closed, they were unable to secure insurance.

Recognizing the terrible conditions on Cypress Island and the victims’ need for justice, we should consider: is that a good outcome? The settlement that ended Secret Harbor was $4 million. This is less than one-tenth of the record-high settlement in Washington State. A single law firm brought 800 of the 1,500 claims filed that year. Premiums are climbing fast for all organizations that serve children. This is particularly true for Skookum Kids, which focuses on child welfare. These increases are linked to changes in the statute of limitations policy. Even if we accept the belief that child welfare was a hellscape in this state through the 70s and 80s, is it a productive societal response to sue out of existence its child-serving organizations in the present? I do not believe it is. I believe we can do better by grappling with the system in a pragmatic way, weighing benefits against costs, making trade-offs rather than dealing in moral absolutism.

I have been working on this issue since 2019, and the most common response I get from policy makers is a sort of casual: if you don’t want to get sued then do a better job. And frankly, I would love to live in a world where that were true. I love being in control of my own fate. I’m confident in Skookum Kids’ programming and risk controls. I often remind people that we’ve never made an insurance claim in our entire history. This is an excellent agency. And the Secret Harbor that I knew was also an excellent agency. What separates Skookum from Secret Harbor is not the quality of the work currently being done in the present; it is the legacy (and liability) of past events under that name. Skookum Kids is twelve years old. I founded the agency and have been here the whole time. Secret Harbor had decades of history—of liability—for which the present-day leaders had no ability to limit, but for which that lawsuit made them responsible.

Secret Harbor is not the only one. Yesterday, I attended a meeting where leaders from three respected agencies shared that they each recently completed six-figure settlements. These settlements are for events that allegedly happened 30 to 40 years ago. The checks will be written by insurance companies—that’s what insurance is for—but the cost will be borne by the entire child welfare system in the form of tighter coverage terms, higher premiums, and a more skittish provider community. Those three organizations will weather the storm, but without a serious change to the environment, it is only a matter of time until another agency goes down because of evil perpetrated before anyone working there was born. No one is saying that child welfare organizations should be exempt from accountability. But accountability is not what is playing out in our courts right now. We’re punishing ourselves for the sins of others. Worse, we’re paying lawyers for the privilege.

How do we fix this mess?

Any effective policy intervention here will involve limiting the tort liability for both the State of Washington and the child-serving organizations within its borders. It must also include some policy that stabilizes the insurance market, ideally by bringing new providers into the state to introduce some new competition for those few still standing. A functional insurance market is simply not possible when anyone can bring a claim, damages are uncapped, and the burden of proof is a simple preponderance of evidence. The cost for an agency to defend against a claim from forty years ago often exceeds insurance limits. So, settlements are usually quick and large. And if we only limit the liability without introducing new participants, we will cement a monopoly capable of driving the same price increases despite reduced liability risk.

We are not the only state with this problem, and others are moving pragmatically to address it. Many states, including several with progressive leadership, have a cap on payouts. Kansas is moving to give child welfare providers qualified immunity which goes too far for my taste. California created a lookback window for historic claims that produced a large but short-term spike in tort claims that is scheduled to close later this year. This sounds smart, but the wave of claims has been too large for its largest insurer to stay in the marketplace.

Ninety percent of California’s child welfare agencies rely on one insurer—Nonprofit Insurance Alliance of California (NIAC). Recently, NIAC said it will leave the California market. This will have disastrous effects. AB 2496, the Foster Family Agency Accountability Act, aimed to intervene. However, it weakened during the law-making process. As a result, NIAC stated it would not change its decision to exit the market. It feels uncomfortable to be rewriting tort policy to suit the preferences of a monopolistic insurance provider, but when the market is allowed to atrophy like this, little other choice remains.

Washington is slightly behind California in terms of acuity. Two or three insurance providers operate here, at least for now. Some of them are limiting their Washington book by not taking new business or non-renewing policies under a given size[4]. What is happening to the south is making its way here. If we act sooner, we can avoid taking dictation from a monopolist during our bill-writing process.

We have seen a little movement over the last two legislative sessions. In 2025, Senator Claire Wilson secured funding for the Office of the Insurance Commissioner to study the market and produce a report. What they found mostly backs up what I and others have said for years. It also includes clear recommendations. These suggestions focus on how to limit liability and start rebuilding the insurance market for organizations that serve children. Unfortunately, it was only published a few days before the start of the 2026 session, meaning few lawmakers had a chance to read and digest its recommendations.

But that did not stop Senator Dhingra from introducing a bill that would require arbitration on most civil claims made against the state, a brave proposal that predictably received criticism from the people who have made a metropolitan living by bringing civil claims against the state. I was excited to see a proposal to limit tort exposure. However, I felt disappointed. This first serious proposal in years only tackled the state’s liability issue. It left community-based organizations to fend for themselves. And it did not pass, so there is a chance to improve it before next session.

If I had a magic wand and I wanted to use it on liability insurance policy. First, I’d cap damages like Oregon does. Next, I’d rewrite the indemnification language in state contracts. This way, liability would accrue to the responsible party, not the contractually dependent one. Finally, I’d set up a victims’ fund with even tighter limits to compensate victims with decades-old claims where defense is impractical and/or the organization or program no longer exists in its harmful form. This combination of reforms would allow us to live up—at least in part—to our value of justice for victims without sacrificing our best service providers to do so.

Limiting institutional liability conflicts with progressive lawmakers’ values. So far, any such proposal has been a nonstarter in Olympia. Any qualifier that follows the phrase ‘victims deserve justice’ feels intuitively wrong. We should ask ourselves: Do we want ideological purity or a child welfare system that works? We cannot have both.

[2] HBH v. State of Washington, 2018

[3] MR v. State of Washington, 2024

[4] Skookum was dropped in that way a couple years ago, and our broker did some yeoman’s work to bring a new provider into the Washington market for us.